How Stock Market Crashes Impact the Housing Market

Wise investors build wealth through diversification, holding a mix of stocks, bonds, and real estate in their portfolios. Diversification spreads risk across investments that may have an inverse relationship, meaning that when one goes down, the other goes up. Historically, although not always, when stocks go down, bonds rise, and vice versa. When bonds rise, their interest rates fall. But the relationship of the stock market to real estate is somewhat less direct. A stock market crash’s impact on housing has more to do with what caused the crash in the first place, combined with other external conditions like jobs and, most recently, a global pandemic.

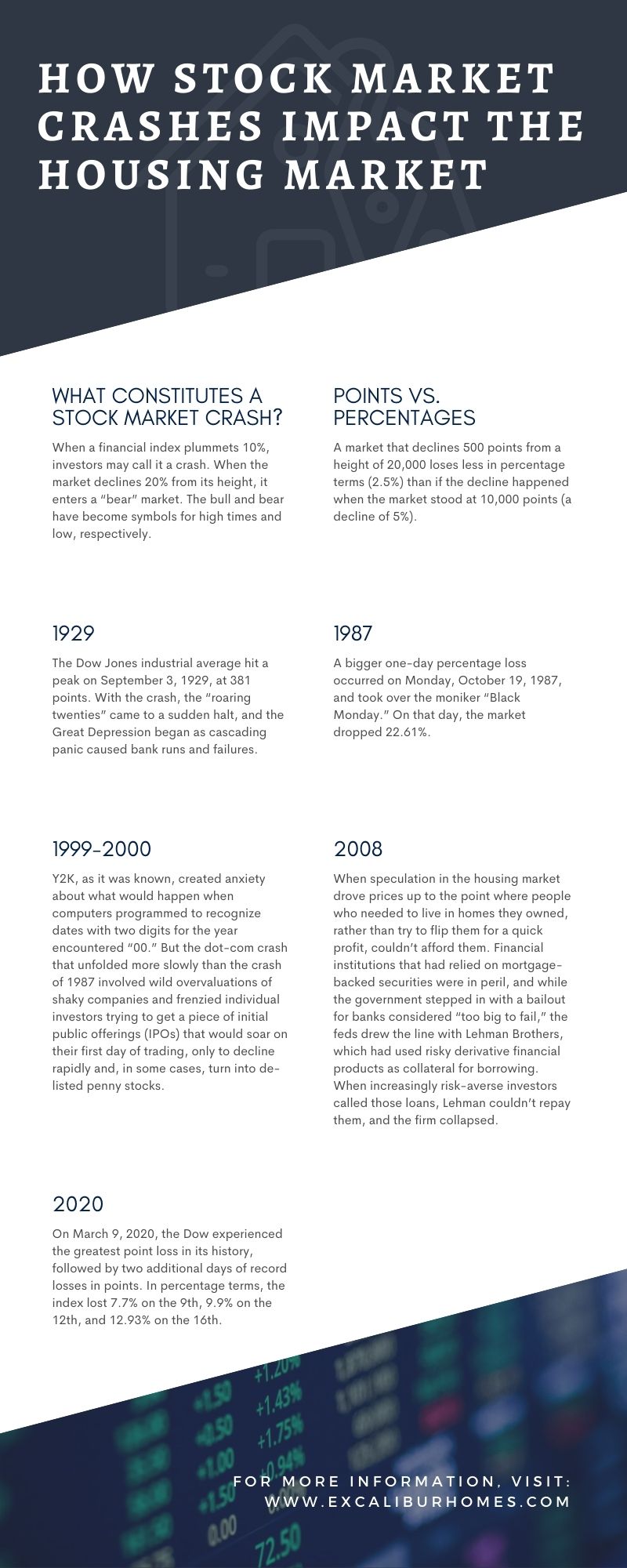

What Constitutes a Stock Market Crash?

Before you can understand the impact of stock market on housing, you must first understand what constitutes a crash. When a financial index plummets 10%, investors may call it a crash. When the market declines 20% from its height, it enters a “bear” market. The bull and bear have become symbols for high times and low, respectively. A bull market is one that just keeps going up, but all investors know that what goes up must come down, eventually—and when stocks come down a lot, investors sell more speculative investments and turn to “defensive” stocks and other investments that tend to hold their value through difficult economic conditions.

Real estate, it would seem, should fall into the “defensive investment” category. After all, people will always need a place to live. But their willingness to buy or sell a home, and their ability to pay a mortgage or afford rent, fluctuates with overall economic conditions—including, but not limited to, the stock market.

Points vs. Percentages

It is important to understand the difference between stock market “points” and percentage gains and losses. A market that declines 500 points from a height of 20,000 loses less in percentage terms (2.5%) than if the decline happened when the market stood at 10,000 points (a decline of 5%). Thus, when the daily news headlines scream that “the Dow lost 750 points today,” that may sound like a huge decline, but to understand the potential impact of the decline, look to the percentage loss.

Crashes sometimes extend over several days as investors begin to panic and sell into the loss, causing further declines.

Below, we look at past crashes and the impact of these stock market crashes on housing prices.

1929

As the most famous crash in U.S. history, the 1929 stock market meltdown saw declines of 13% on October 28, 1929, the first “Black Monday,” followed by another decline of 12% on “Black Tuesday,” October 29, 1929. The Dow Jones industrial average hit a peak on September 3, 1929, at 381 points. With the crash, the “roaring twenties” came to a sudden halt, and the Great Depression began as cascading panic caused bank runs and failures.

Historians point to overconfidence from the booming economy of the ‘20s, the abundance of easy credit and buying on “margin” (borrowing to finance investments), an oversupply of goods and agricultural products, and a sudden increase in interest rates as primary causes of the crash. Many people who couldn’t afford to lose, lost everything they had, including their jobs and their homes. This stock market crash had a huge impact on housing and led to a prolonged slump in real estate prices—just one part of the overall economic disaster that was the Great Depression.

1987

A bigger one-day percentage loss occurred on Monday, October 19, 1987, and took over the moniker “Black Monday.” On that day, the market dropped 22.61%. Speculation, margin, and highly leveraged corporate buyouts and takeovers built on shaky financing vehicles like junk bonds, all played a role. The crash of 1987 was the first time computerized trading played a part in accelerating selling and related losses. Market leaders imposed “circuit breakers” that could stop trading if it got out of control. This stock market crash’s impact was minimal; the market recovered from this loss relatively quickly. Investors did turn to defensive bonds, causing bond prices to rise and interest rates to fall and making mortgages cheaper. Fewer individual investors felt the effects of the crash of 1987, and the real estate market was only temporarily and regionally (as in New York City commercial real estate) impacted.

1999-2000

Y2K, as it was known, created anxiety about what would happen when computers programmed to recognize dates with two digits for the year encountered “00.” But the dot-com crash that unfolded more slowly than the crash of 1987 involved wild overvaluations of shaky companies and frenzied individual investors trying to get a piece of initial public offerings (IPOs) that would soar on their first day of trading, only to decline rapidly and, in some cases, turn into de-listed penny stocks. Most of those individual investors, however, were wealthy people who could endure the loss. The bursting of the dot-com bubble had little effect on ordinary retail investors, as they found themselves locked out of participating in the speculative boom in the first place.

2008

Unlike the dot-com boom of 2000, the housing bubble that burst in 2007-2008 hit lower-income people the hardest. Easy credit and subprime lending played a big part. No-documentation loans made to people who couldn’t afford them and may not have understood the impact of the financial obligation they were taking on were then packaged into “mortgage-backed securities.” When speculation in the housing market drove prices up to the point where people who needed to live in homes they owned, rather than try to flip them for a quick profit, couldn’t afford them. Housing prices began a decline in 2007, and people who took out loans they couldn’t afford began to default. This, in turn, affected the value of mortgage-backed securities, turning them into junk investments. Financial institutions that had relied on mortgage-backed securities were in peril, and while the government stepped in with a bailout for banks considered “too big to fail,” the feds drew the line with Lehman Brothers, which had used risky derivative financial products as collateral for borrowing. When increasingly risk-averse investors called those loans, Lehman couldn’t repay them, and the firm collapsed.

2020

On March 9, 2020, the Dow experienced the greatest point loss in its history, followed by two additional days of record losses in points. In percentage terms, the index lost 7.7% on the 9th, 9.9% on the 12th, and 12.93% on the 16th. The market has continued to swing with great volatility, and recent data for the second quarter of 2020 indicates the worst decline in gross domestic product (GDP) ever recorded—nearly 35%. The March declines were fueled in part by trade wars, but much more by the impact of the coronavirus pandemic. Record unemployment, bankruptcies, and a big drop in demand for oil all signal a possible major recession.

The impact of the stock market on housing prices in 2020 is still up in the air. Some suburban areas have seen a housing boom as buyers with means flee high-density cities in pursuit of single-family homes with yards and plenty of space. At the same time, people who might have been considering selling their homes are delaying listing them, reducing supply. Stock markets and housing markets are affected by consumer confidence, interest rates, and lending requirements. In the COVID-19 crisis, some businesses like hospitality and airlines and their workers have suffered badly, while some tech industries that carried on seamlessly while employees worked from home posted gains.

Real estate investors in markets like Atlanta, with a higher population of tech and professional workers and industries, should weather this crisis with stable tenants who can continue paying rent. Suburban markets will see interest from buyers and renters fleeing dense population centers for wide-open spaces, as they realize they don’t have to live in the city to work from home. Rental property management companies in Atlanta and real estate agents can help eager tenants find available homes and help investors buy or sell income properties. Services include screening tenants, collecting rents, and taking care of maintenance through economic downturns as well as the good times.

Wise investors build wealth through diversification, holding a mix of stocks, bonds, and real estate in their portfolios. Diversification spreads risk across investments that may have an inverse relationship, meaning that when one goes down, the other goes up. Historically, although not always, when stocks go down, bonds rise, and vice versa. When bonds rise, their interest rates fall. But the relationship of the stock market to real estate is somewhat less direct. A stock market crash’s impact on housing has more to do with what caused the crash in the first place, combined with other external conditions like jobs and, most recently, a global pandemic.

Wise investors build wealth through diversification, holding a mix of stocks, bonds, and real estate in their portfolios. Diversification spreads risk across investments that may have an inverse relationship, meaning that when one goes down, the other goes up. Historically, although not always, when stocks go down, bonds rise, and vice versa. When bonds rise, their interest rates fall. But the relationship of the stock market to real estate is somewhat less direct. A stock market crash’s impact on housing has more to do with what caused the crash in the first place, combined with other external conditions like jobs and, most recently, a global pandemic.